Why won't Bitcoin go up?

And some plausible explanations around why it went down so much this past week.

Normal people only want to talk about the price of bitcoin at two moments: when it has gone up a lot or when it has gone down a lot.1

This past week it went down a lot.

But if you zoom out a bit, price is actually up.

And if you zoom out to all time, it’s up a ton!

But there is no time machine2 available for you to go back to 2010 and dump your life’s savings into Bitcoin and net an easy 100000x return. So let’s focus on all the things that happened this past week.

First, some quick disclosures: 1/ There are a lot of people much smarter than me you should be asking these things, if I knew the answers with absolute certainty I would be running a hedge fund instead of working in venture capital. 2/ In case it isn’t obvious, this is not financial advice3.

This has happened before

Bitcoin has had many periods of volatility where it experienced sharp declines, it is a bit difficult to even describe or categorize them.

To attempt to place the most recent price slide:

Post-Futures Bubble Burst in Dec 2017: 65% decline over 51 days

Terra/Luna Contagion & Cascade in May 2022 : 56% decline over 44 days

China Crypto Ban & Tesla Reversal in Apr 2021: 53% decline over 35 days

Covid Panic in Mar 2020: 47% decline over 4 days

Whatever you call the last few weeks: 43% decline over 10 days

But things are a bit different now

I love Bitcoin4 but the price of Bitcoin =/= a measure of people using crypto or a view into adoption of crypto.

We’ve made a lot of progress as an industry:

Basic access is easier by the day, basically everyone with a brokerage account has at least had access to Bitcoin ETFs for years now.

Gary Gensler’s era of regulatory through enforcement that hampered growth has come to an end.

Congress passed the Genius Act outlining rules for Stablecoins.

If we can manage to keep the government open they will likely pass the Clarity Act outlining more general market structure rules.

To try to judge all of that by the price of Bitcoin is the wrong way to look at it. The problem is that the Bitcoin and Crypto narratives remain intermingled even though they have largely become decoupled.

There are a number of metrics beyond using Bitcoin price as a proxy that better explain industry progress:

Stablecoin market cap is over $300B (tokenized dollars represent the strongest example of crypto product market fit after trading5)

Average aggregate blockchain transactions per second is ~4,300 (still smaller than the card networks but rapidly closing the gap6)

15% of the global internet population now holds crypto

Prediction market volume is up over 300% YoY7

To quote Chris Dixon, “…the core idea was never that every crypto application would emerge all at once, or that finance wouldn’t come first. The core idea was — and remains — that blockchains introduce a new primitive: the ability to coordinate people and capital at internet scale, with ownership embedded directly into the system.”

Back to Bitcoin though…

Bitcoin has not (yet) turned into the ultimate store of value

Key caveat being yet8. A lot of the very high expectations around Bitcoin are that it turns into the ultimate hedge against the current financial system’s obvious problems (printing money with abandon, endless debt, etc.).

For a long time it felt like Bitcoin was on this path but for the last few years, the opposite has happened. Bitcoin really just trades like a levered risk-on asset and correlates a lot to where tech stocks are trading, (except for AI but we will get to that in a second). Instead, gold has won the hearts and minds as the safe haven asset of choice9. The simplest explanation is that Bitcoin is seen as a tech thing. If you are like “yeah tech is going to have a good run for a while you buy some Bitcoin” and if the opposite is true you sell some10.

But then there is AI. The world is in a weird place right now because of AI. Or more specifically, how the world views valuations of public companies and tech stocks is in a weird place because no one is certain what is going to happen next with AI.

Most of the big tech stocks that aren’t pure AI are SaaS companies struggling to transition in this era of AI (Saleforce, Shopify, Figma, etc). SaaS stocks are getting hammered and Bitcoin is bucketed in with those for enough people that for the time being its price largely moves as those move. Or at least that is the simplistic way to view it all.

Last week, Anthropic released a new model (Opus 4.611) which triggered slightly more than usual hang wringing about AI’s impact on absolutely everything. On top of a bunch of other factors (more below) happening at the same time, the market reacted in a negative way.

Yesterday during the Super Bowl, Anthropic running a series of highly provocative ads poking at Open AI, their main rival. One example:

This has been pretty choreographed for the past few weeks, to the point where it seems like OpenAI should have had time to prepare some sort of response to drop into the news cycle following the Super Bowl to try to push this out of people’s minds. If they drop big enough news, I could easily see this cycle of driving everything tech related further downward, repeating itself.

But again, it’s not that simple. Behind the simplistic “Bitcoin moves with risky tech related things” idea there are a lot more complicated things happening. The world of finance is big and there is a lot of money changing hands. Its my view that there is rarely ever a single causal factor, its the confluence of many different events.

Other plausible factors

Here is a rundown of the most repeated “other” factors and my quick take on how much each one mattered. The unsatisfying but likely correct answer is probably some combination of all of these things plus the correlation described above.

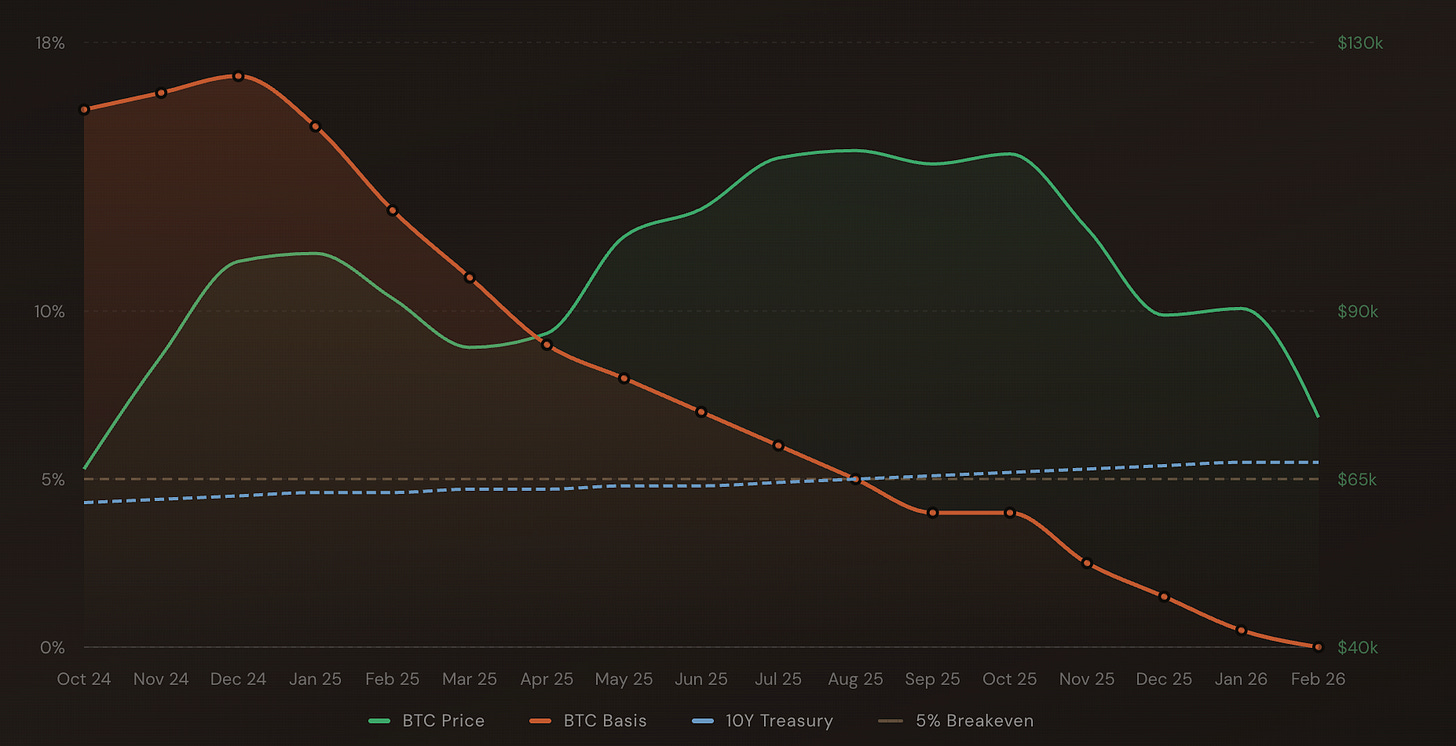

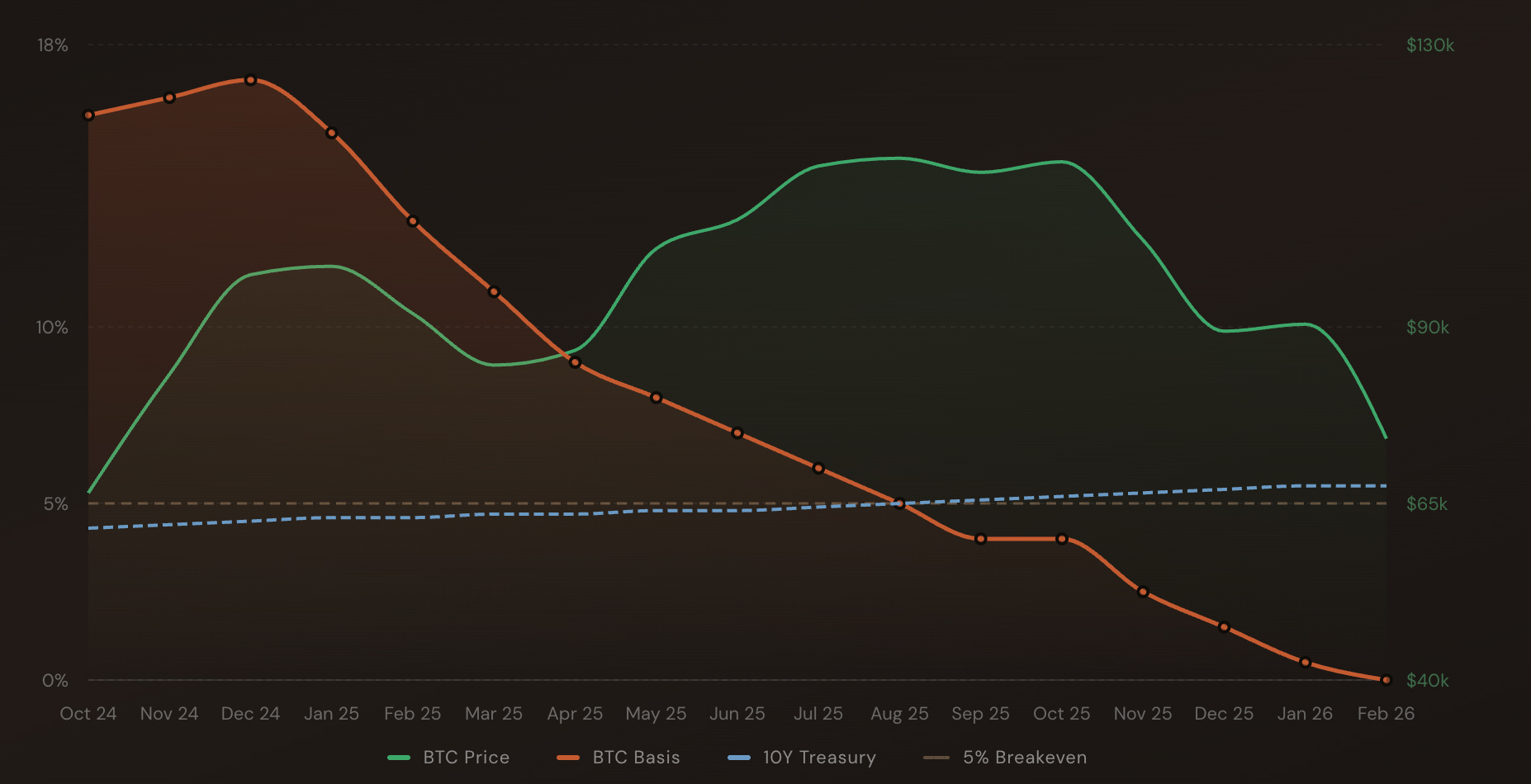

Basis trade unwind:

A basis trade is when big investors buy bitcoin in one place (like an ETF) and simultaneously sell bitcoin futures in another place, pocketing the small price difference between the two like a coupon. When that price gap shrinks and the trade stops being profitable, everyone rushes to close both sides at once, which means a ton of selling hits the market all at the same time. The profitability of the basis trade has definitely decreased, but it was doing so long before the Bitcoin price side began.

DAT contagion:

DATs (Digital Asset Treasury companies)12 are public companies, like Strategy (formerly MicroStrategy), that loaded up their corporate balance sheets with bitcoin instead of keeping normal cash reserves. When bitcoin’s price drops, these companies’ stocks tank too, which can force them to sell bitcoin to stay solvent, which pushes the price down further, which hurts more DAT companies, creating a nasty domino effect that spills into traditional stock markets. Strategy is the largest of these by far and so far they haven’t sold any holdings, but you could see how this might be a factor in the future depending on the the terms of debt. Maybe “Misguided fear of DAT contagion” is more accurate.Bessent testimony related to the new Fed Chair appointment:

During congressional hearings about new Fed Chair nominee Kevin Warsh’s views, Treasury Secretary Scott Bessent was asked about Bitcoin. If you look at the exact testimony all the pull quotes got taken out of context and everyone jumped to conclusions. Maybe slightly related but it doesn’t seem like sophisticated actors holding significant amounts of Bitcoin would overreact so much.Yen carry trade:

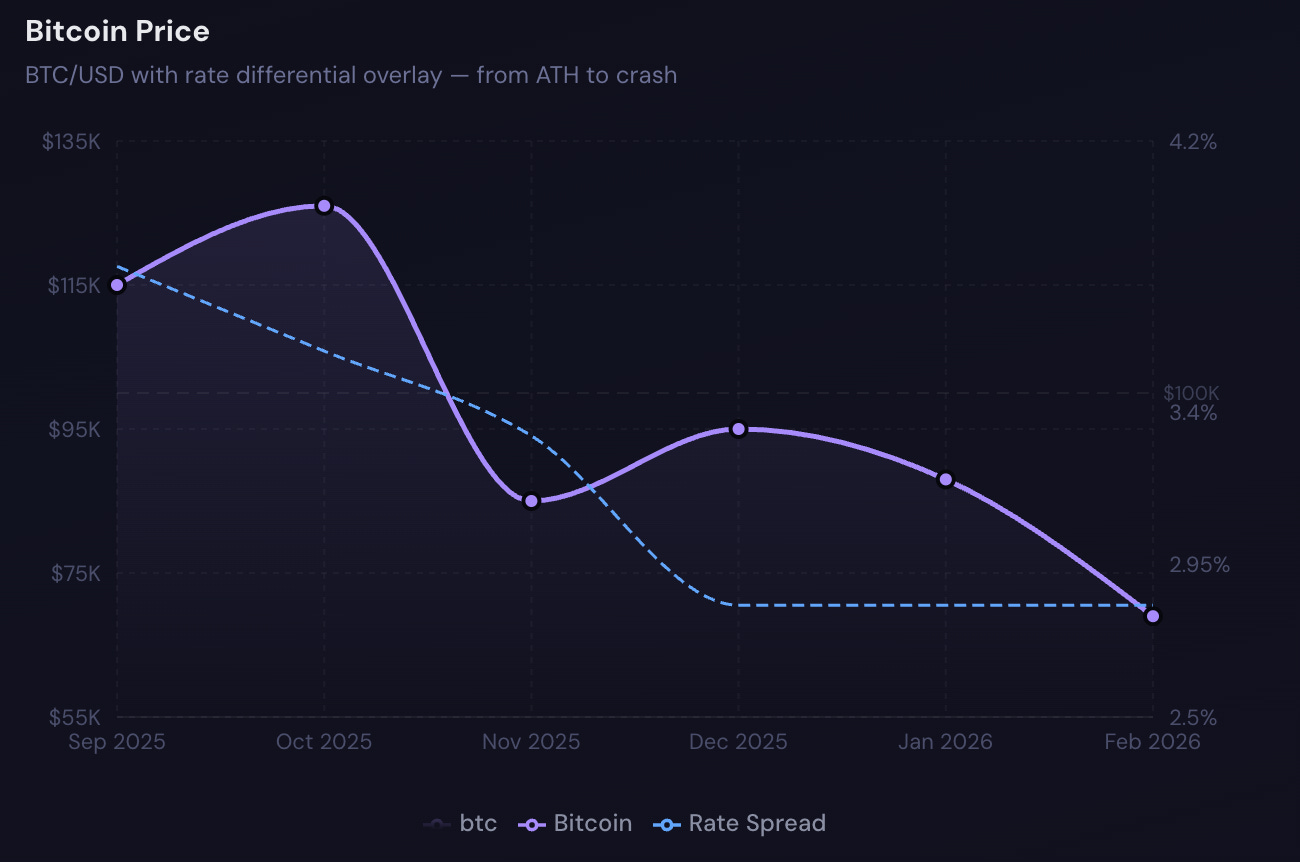

The yen carry trade is when investors borrow money cheaply in Japan (where interest rates are super low) and then invest that borrowed money into higher-yielding assets elsewhere, like U.S. stocks or crypto, to pocket the difference. When Japan’s interest rates suddenly rise or the yen gets stronger, those investors have to scramble to pay back their now more expensive loans by selling off whatever they bought, including bitcoin. Of the four other factors this seems like the most significant to me13.

Seems plausible? this graph is grossly over simplified

Where does value accrue going forward and why?

The question to ask going forward is where will value accrue in the future? I am even less certain of the answers here, so here is some speculation. Consider these a jumping off point to think about for yourself.

The case for Bitcoin going up a ton: Long term limits on supply ultimately overcomes all other factors.

The case for Solana going up a ton: Wins the war for being the super fast high throughput L1 for everything.

The case for Eth going up a ton: Momentum and mindshare cause it to be the everything L1 and they figure out gas fees somehow.

The case for Sui going up a ton: All of high frequency trading is on chain and this is the place it happens.

The case for Polygon - It’s now super undervalued and they win on being the home of all blockchain payments.14

The case for Hype - Hyperliquid remain the dominant DEX for Perps volume and continues to print money they use to buy the token and make the price go up.

Finally, Coinbase stock - Suddenly it is a value buy and they win the war to be the everything bank.

I’ll likely spend the next week or so digging into each.

I’m only fully certain of two things:

DAT exposure to Bitcoin is bad and pointless. Stay away from Strategy stock.

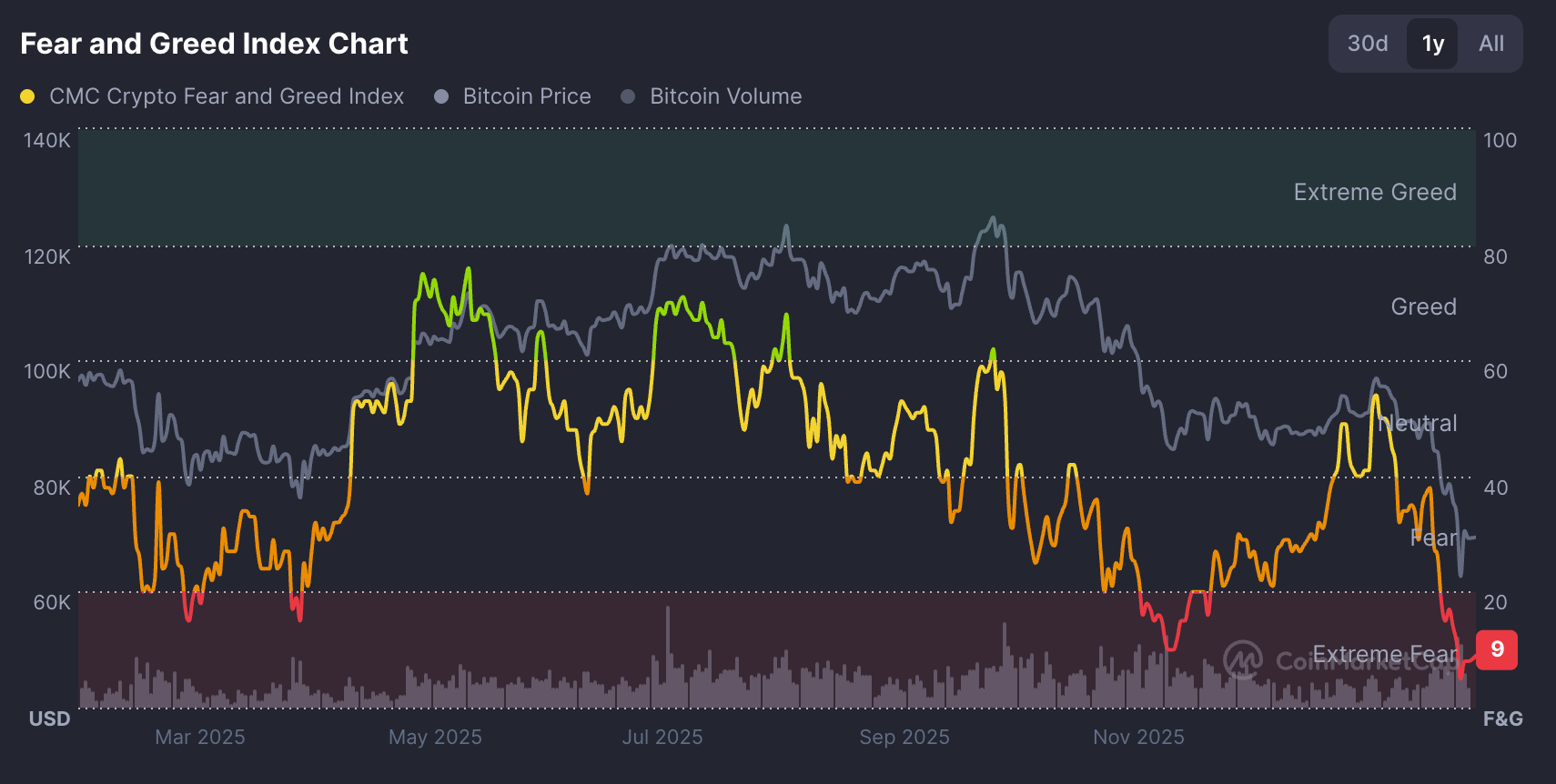

Sentiment is basically at an all time low

As always, if anyone else has theories, post in the comments! Thanks.

Actually normal people don’t ever want to talk about it. The joke at our office is that there are only two clear market signals. Market bottom = random friends text you about the price of Bitcoin being low. Market top = random friends text you about the price of bitcoin being high.

This reminds me of one of the more out there Satoshi theories which always makes me chuckle: Satoshi is actually a sentient AI from the future who created a time machine. The sole purpose of the time machine is to use it come go back in time to invent crypto in a way that garners maximum attention and most importantly demands tons of compute. Doing all of this helps lay the infrastructure groundwork for AI and accelerates the timeline for AGI. The more you think about it the more ways it breaks down but fun to consider.

Nothing in this blog post is financial advice. I am not a financial advisor. I am a person who is still holding the Scottie Pippen meme token because I met him in person and he seemed like a nice guy. You should not make money decisions based on anything I say, write, or vaguely gesture at. If you do, that’s between you and your bank account, and I wish you both the best. For actual financial guidance, please consult a licensed professional — someone who owns a real briefcase and knows what a “fiduciary” is without Googling it.

To be clear I am very pro Bitcoin but not a maxi. I have responsibilities called: wife, kids, mortgage. I’m not dumping every penny of my net worth into Bitcoin. A fun fact that will probably result in severe consternation in my household: I recently did the math on an alternative universe where I took the down payment for my apartment and instead went all in on Bitcoin. The result even at today’s prices is a nice nine figure payday. Bit of a silly exercise, all investments looks good in hindsight. I’m also the guy who spent the equivalent of a million dollars on a ski trip I funded by selling some Bitcoin back in 2015. These things happen. 🤷

Or the “magic internet casino machine” as folks like to call it. These folks are not wrong.

Not the most perfect comparison, but to me this represents directional growth towards crypto rails being resilient enough to replace other rails one day, whether it’s the card networks, ACH, wires, etc. This is an important prerequisite for further transformation of parts of the financial services industry.

Polymarket and prediction markets wouldn’t exist without crypto. Crypto being the infrastructure layer enabling entirely new business categories is not talked about enough.

I think this is inevitable given the inherent constricted supply built into the protocol, but that’s not the same as saying if you buy today this will be the greatest investment of all time. For a long time if had you bought Bitcoin this would have been true. But investments are relative to time scale. If you had bought exactly four years ago, IRR would be ~14% which is pretty good but there are lots of places you could have earned a better return. If you are expecting a wild 10,000x return your entry point needed to be a lot sooner. There is a world where both of these things are true: Bitcoin is the ultimate store of value and it was a pretty great return but not the best return ever. Example: If Bitcoin price goes from here to $1M but it takes 10 years, that’s a 30% annualized return. Pretty great but it won’t be the best possible return.

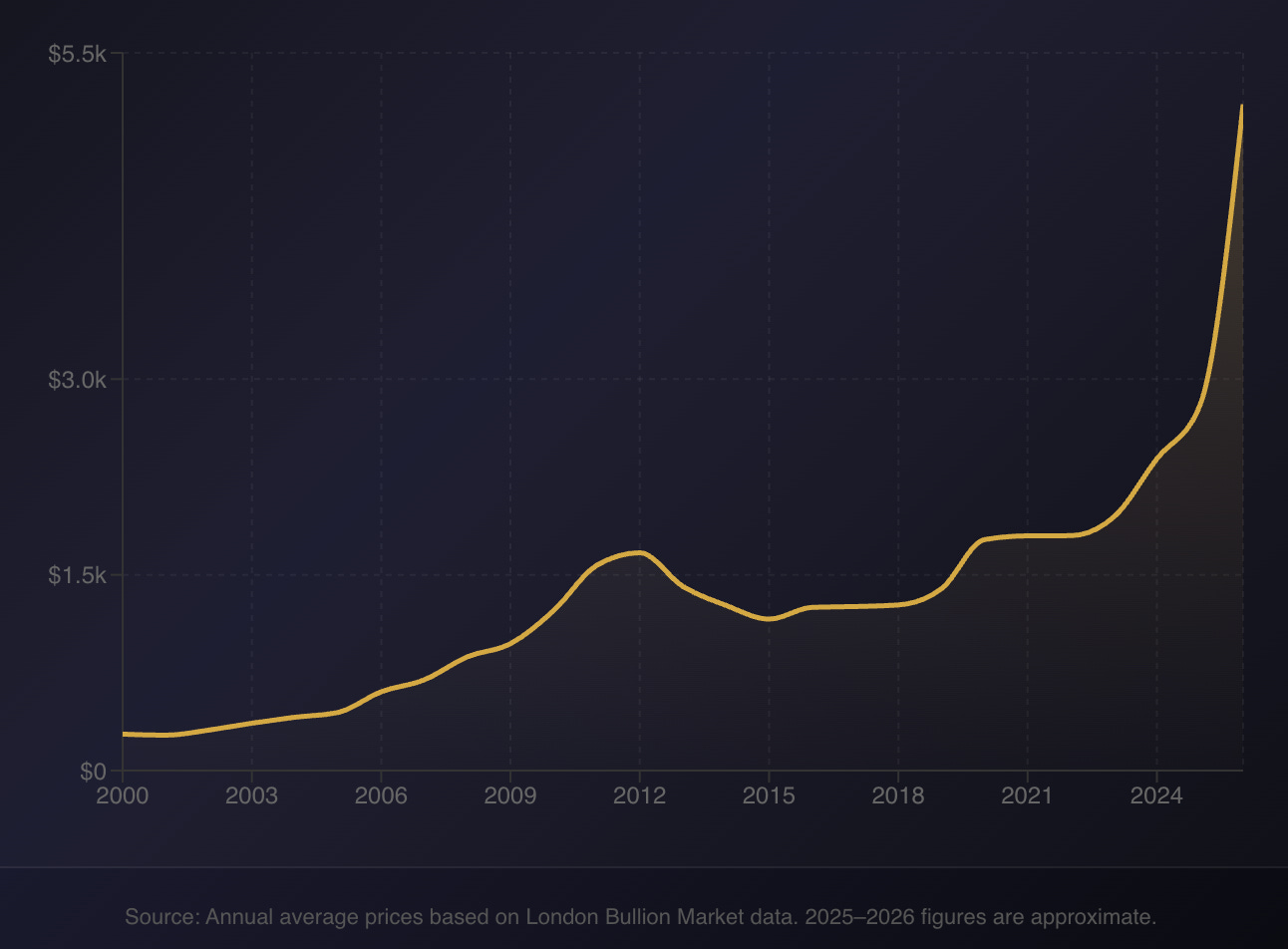

I think this proves to be pretty short term. Gold is a great asset for basically all the same reasons as Bitcoin but it looks like governments, namely China, trying to pull back on reliance on the US dollar is a major factor.

This happens at scale and automatically through indices, but you get the idea.

If anyone can provide me with an explanation of how and why the big AI companies version these model, I am very interested. It seems largely nonsensical to me.

Also a really smart market structure person I asked about this said, “In my career yen carry unwind has always been bigger than we thought.”

People like to poke at Polygon but I have a lot of respect for them going ALL IN on payments vs trying to be everything for everyone. They’ve also made a lot of smart hires and acquisitions recently.