Which is the third best stablecoin?

Or possibly a new way to think about which one is actually best

As a continuation of my last post about misconceptions around stablecoins, I wanted explore this idea that market cap isn’t really the metric we should be grading these things on. I’m curious how one might evaluate which is the third best stablecoin or if you were to ignore the AUM1 numbers of Circle and Tether if there is actually a different stablecoin that should be considered number one.

This is suddenly even more relevant as Tether contemplates raising money at a $500B valuation2 which is a topic for another day.

From what perspective?

Worth noting the answer to the question really depends on your perspective which could be:

Investors - how should I think about investing in incumbents or future upstarts

Users - which stablecoin should I use?

Founders / operators - which stablecoin(s) should my business bet on or support?

General prognosticator - what is going to happen with stablecoins?

For purposes of this post, I’m not going to differentiate further. You’ll have to just decide for yourself with parts matter from your perspective.

Why isn’t market cap the best metric for evaluating stablecoins?

To be clear, market cap still might be the best metric3. After all, it is a simple proxy for most other metrics like revenue4 or liquidity. Market cap is what the media uses, all charts / leaderboards default to it, etc.

The problem is that market cap is currently more of an indication of who was early. In a world where ~1% of dollars are tokenized and stablecoins themselves are likely still super early, this might not matter long term. There is also the case of BUSD5 which at its peak had a market cap of $26B but today is only at $368M. Just because things are going great for Circle and Tether today doesn’t mean that will continue to be the case.

It is still be anyones game to win6.

What other metrics might matter?

So if market cap doesn’t mean best, what is the reasonable universe of other metrics to consider? The ones I quantify further on are:

Transaction count

Transaction volume

Active addresses

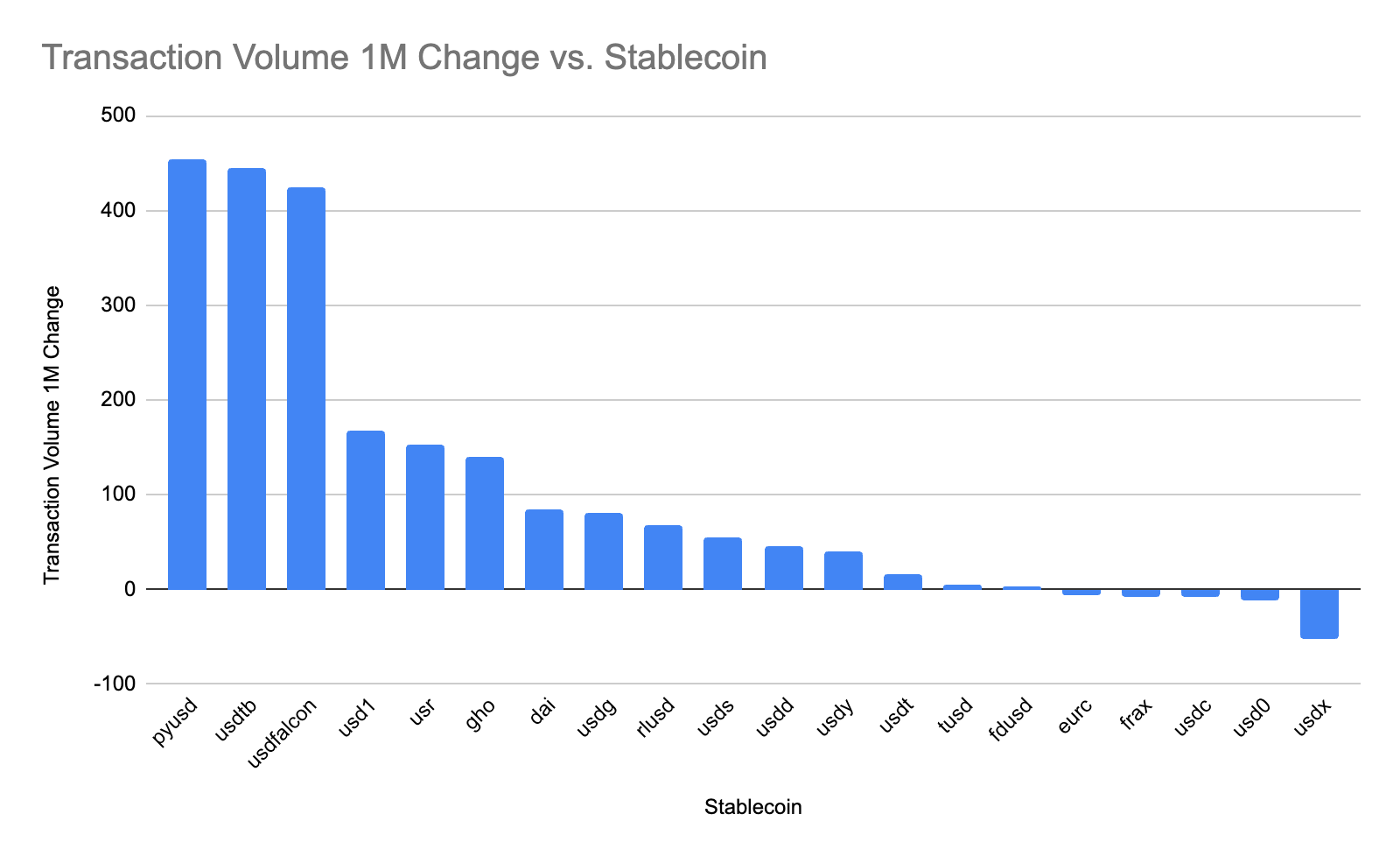

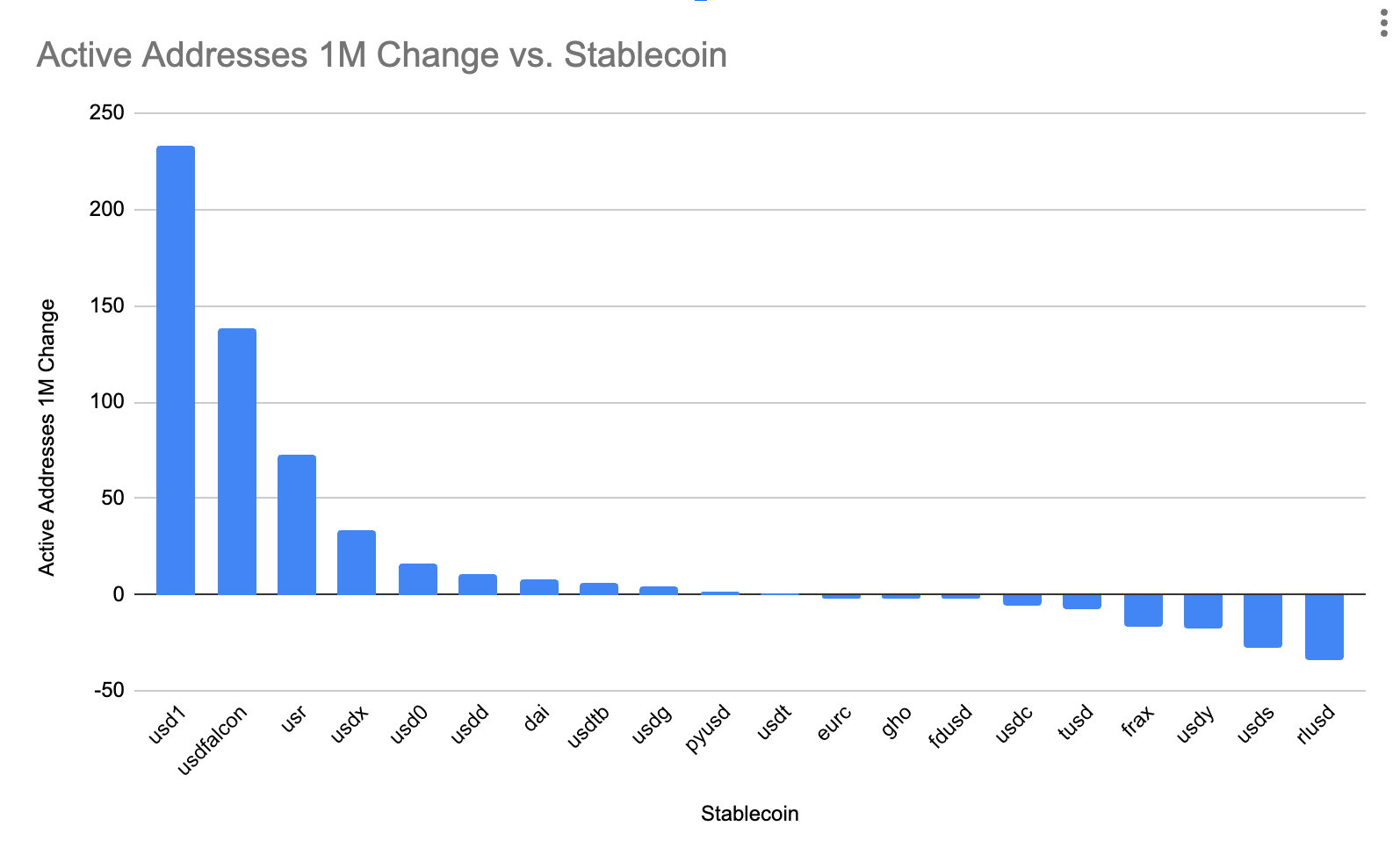

Growth rate (% increase of the above)

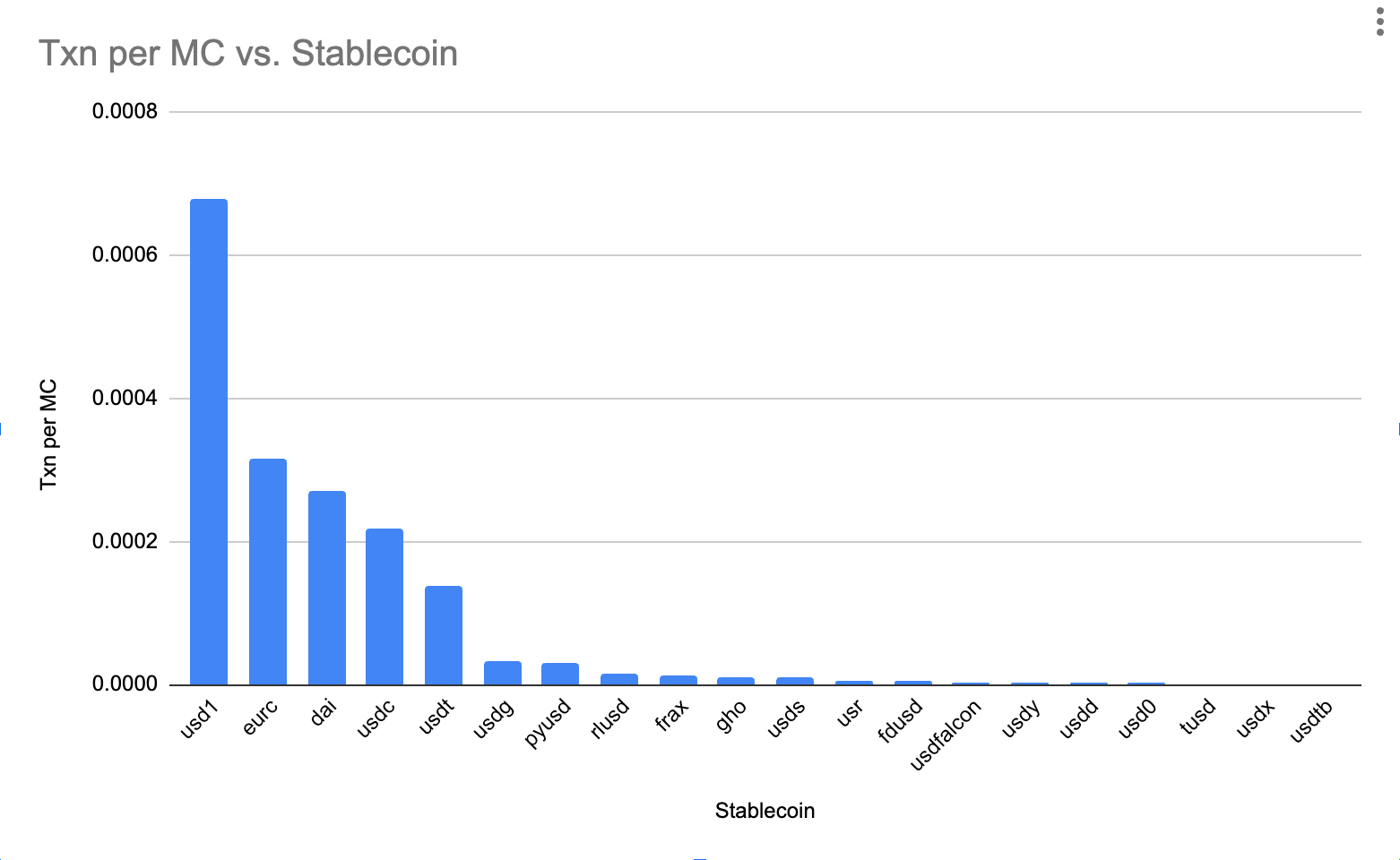

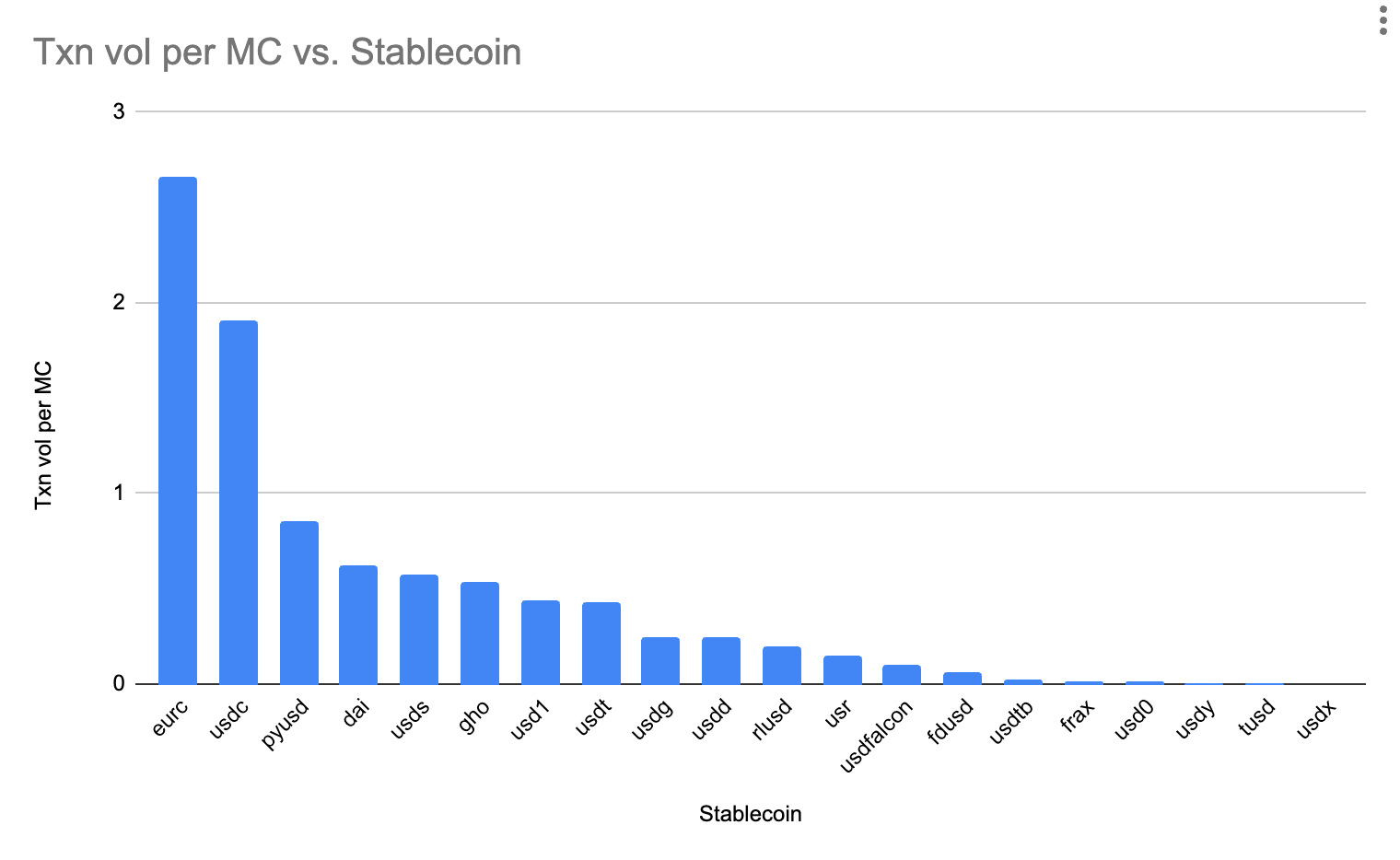

Ratios (comparing the above relative to market cap)

There are also possible metrics which cannot be quantified easily7 but probably matter:

Revenue8

Partnerships9

Regulatory status10

Brand11

Peg stability12

Backing assets13

Transparency on the above14

Smart contract usage15

Yield amount given to end users16

Costs17

Spot trading listings / spot trading volumes18

Interestingly the three things that probably don’t matter on per stablecoin basis are transaction throughput, speed of transfer and cost to transfer. These are all dependent on the chain19 the stablecoin is issued on. This is interesting because the barriers to entry to issue a stablecoin on an additional chain are fairly small. The conclusion I come to is that for a lot of use cases where these things matter (i.e. payments), the stablecoin piece itself largely doesn’t matter. Or said another way, at this stage the stablecoin specific characteristics aren’t materially different enough to matter.

Finally a note on methodology for everything that follows. I’m ignoring all stablecoins with less than $250M in market cap. I used Artemis20 to source all data. I recognize that a better way to do this is to build a dashboard and track over a longer period of time21, this probably skews a bit towards which ones had a particularly good week this week. I’m ignoring BUSD (it is winding down) USDe (backing assets and yield are too different), BUIDL (metrics are too funky). This conveniently leaves us with 20 Stablecoins (18 not counting USDC / USDT) to compare.

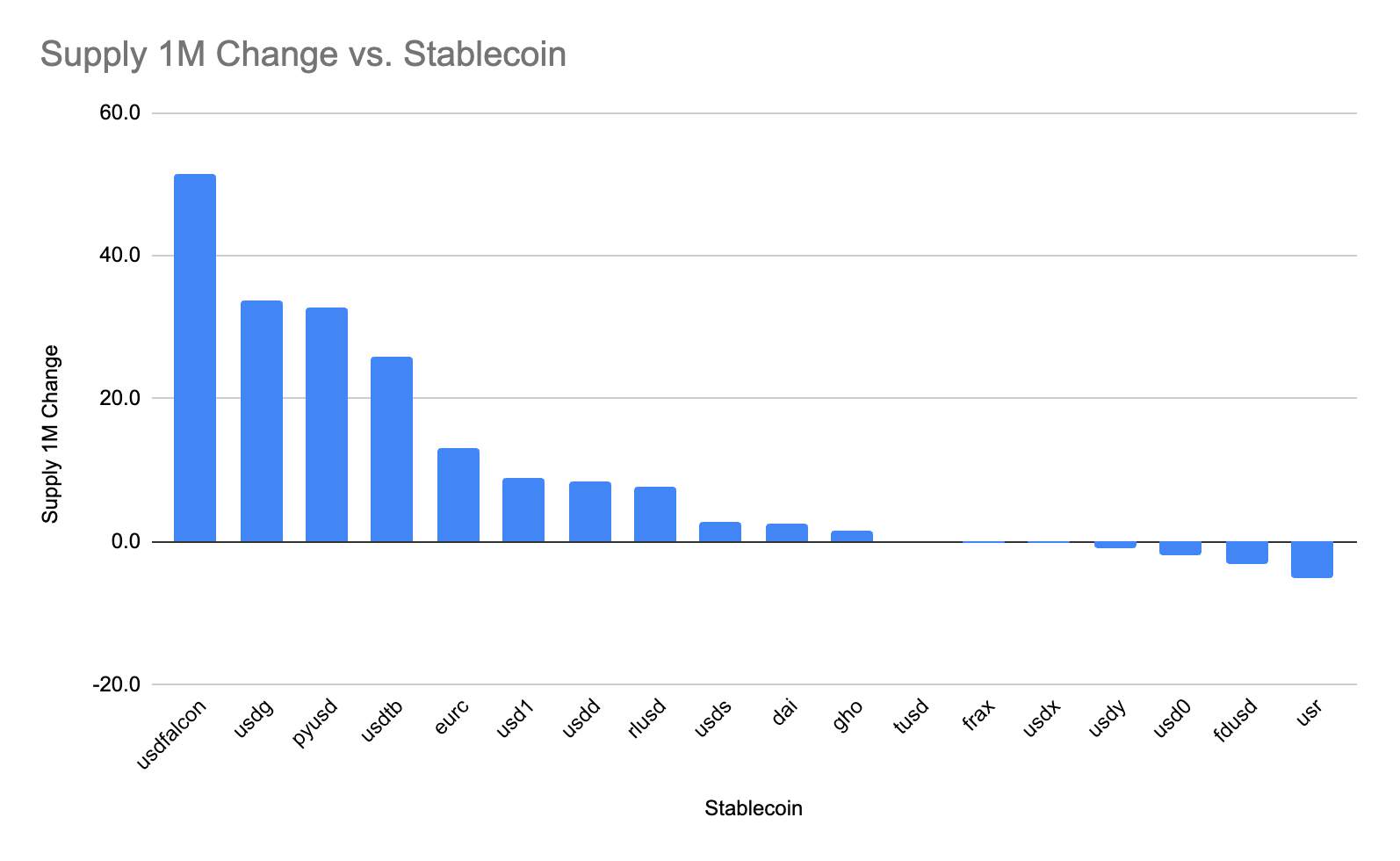

What about market cap growth?

Even though the premise here is that market cap probably isn’t the right metric, it’s worth quickly taking a quick look at market cap growth of the non-USDC / non-USDT stables. Several of these are on pace to overtake USDC in market cap in about a year22.

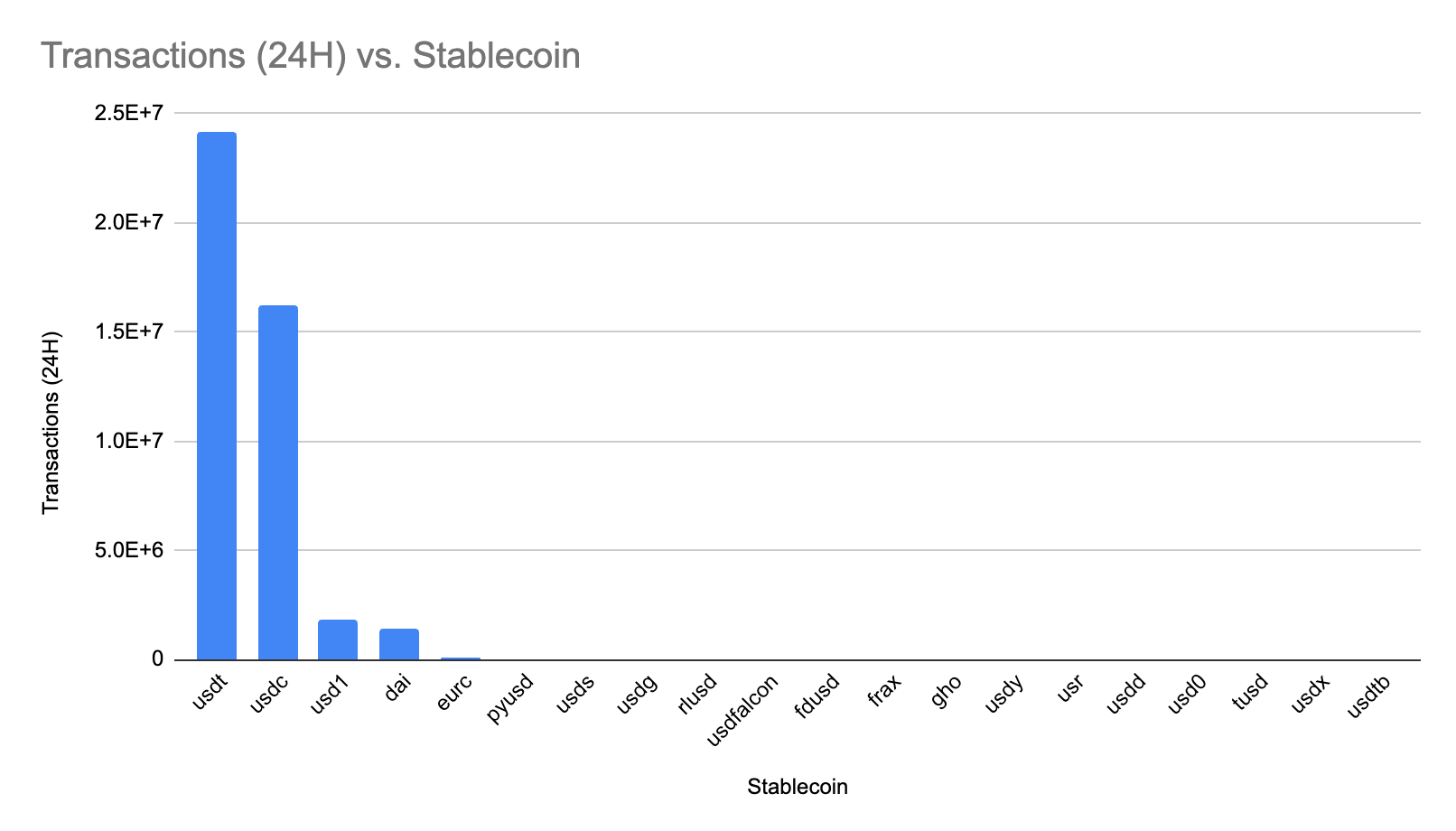

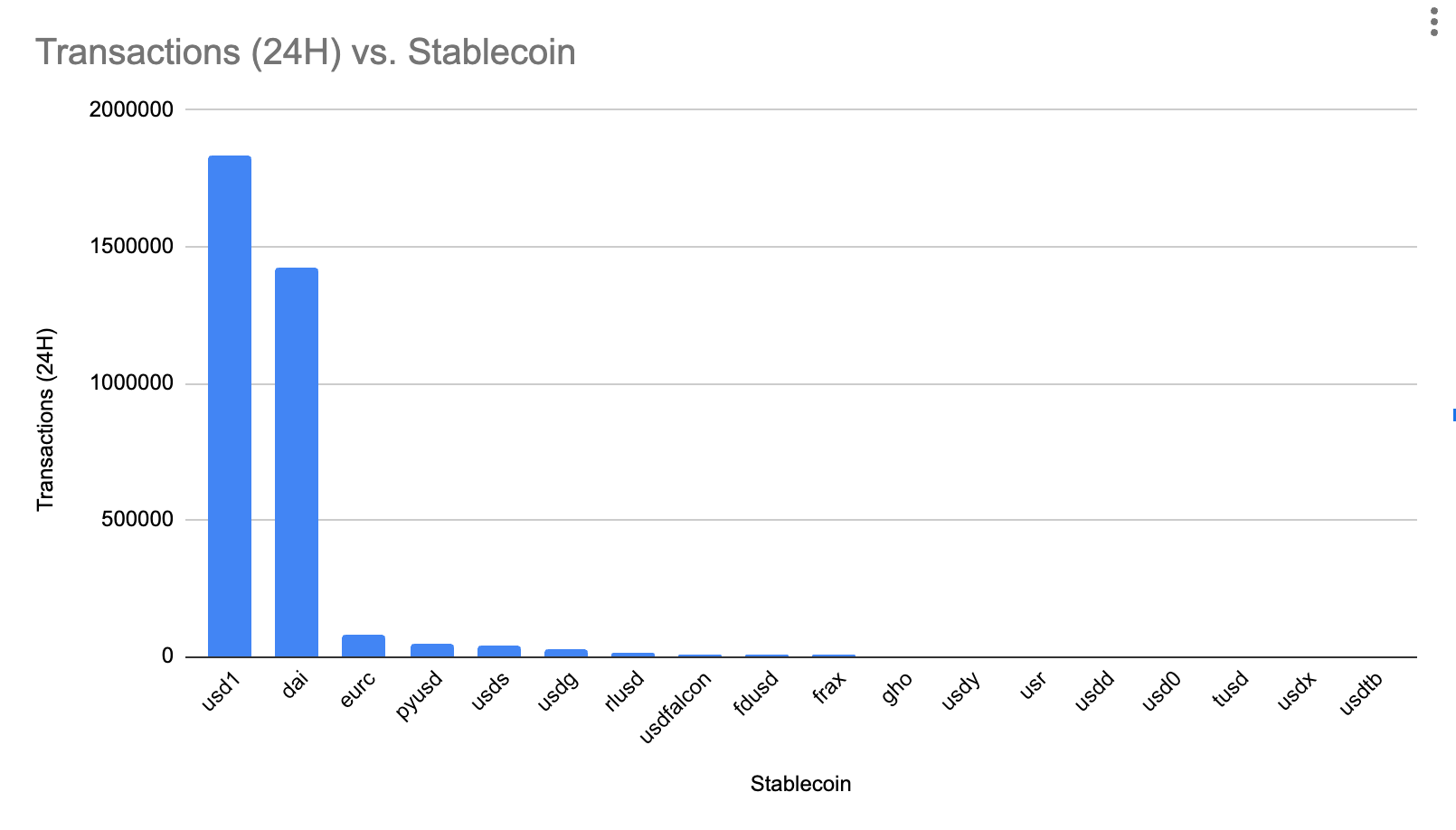

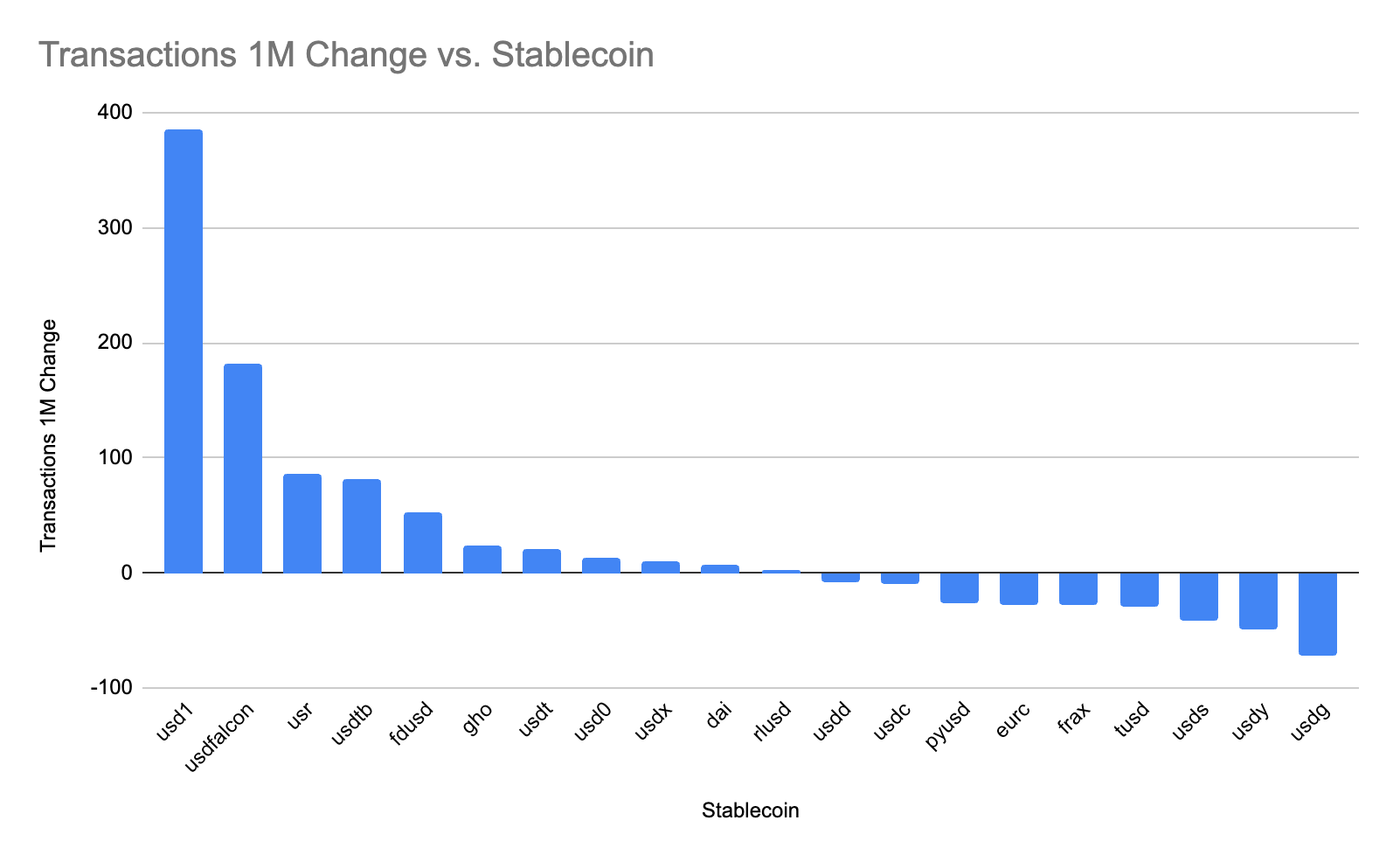

What happens if we use transaction count?

In this scenario, USD1 and DAI are competing to be third biggest. This still feels like a bit of an apples to oranges comparison that starts to uncover use cases more than anything. Some use cases create a lot of transactions some don’t. Neither is good or bad necessarily.

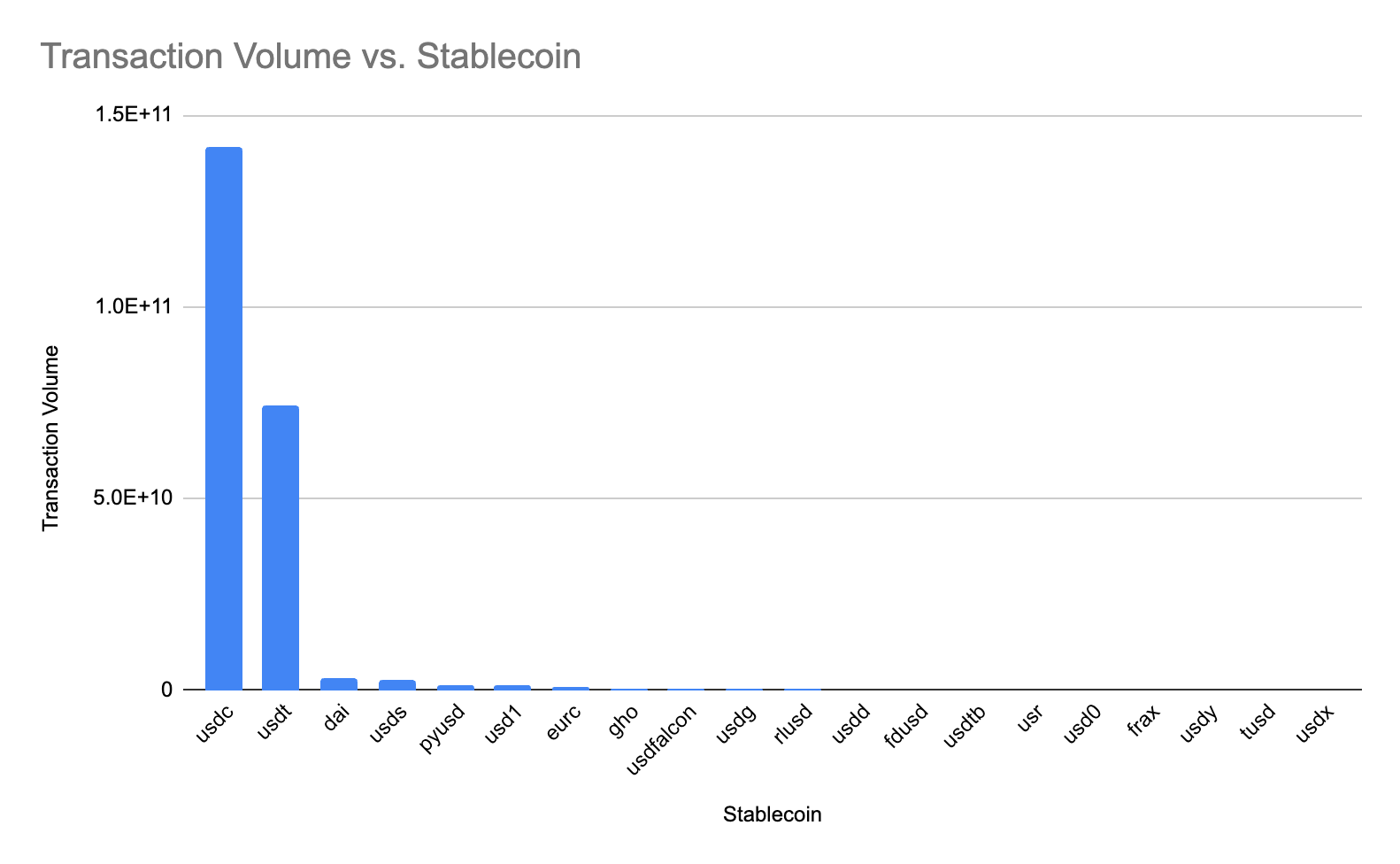

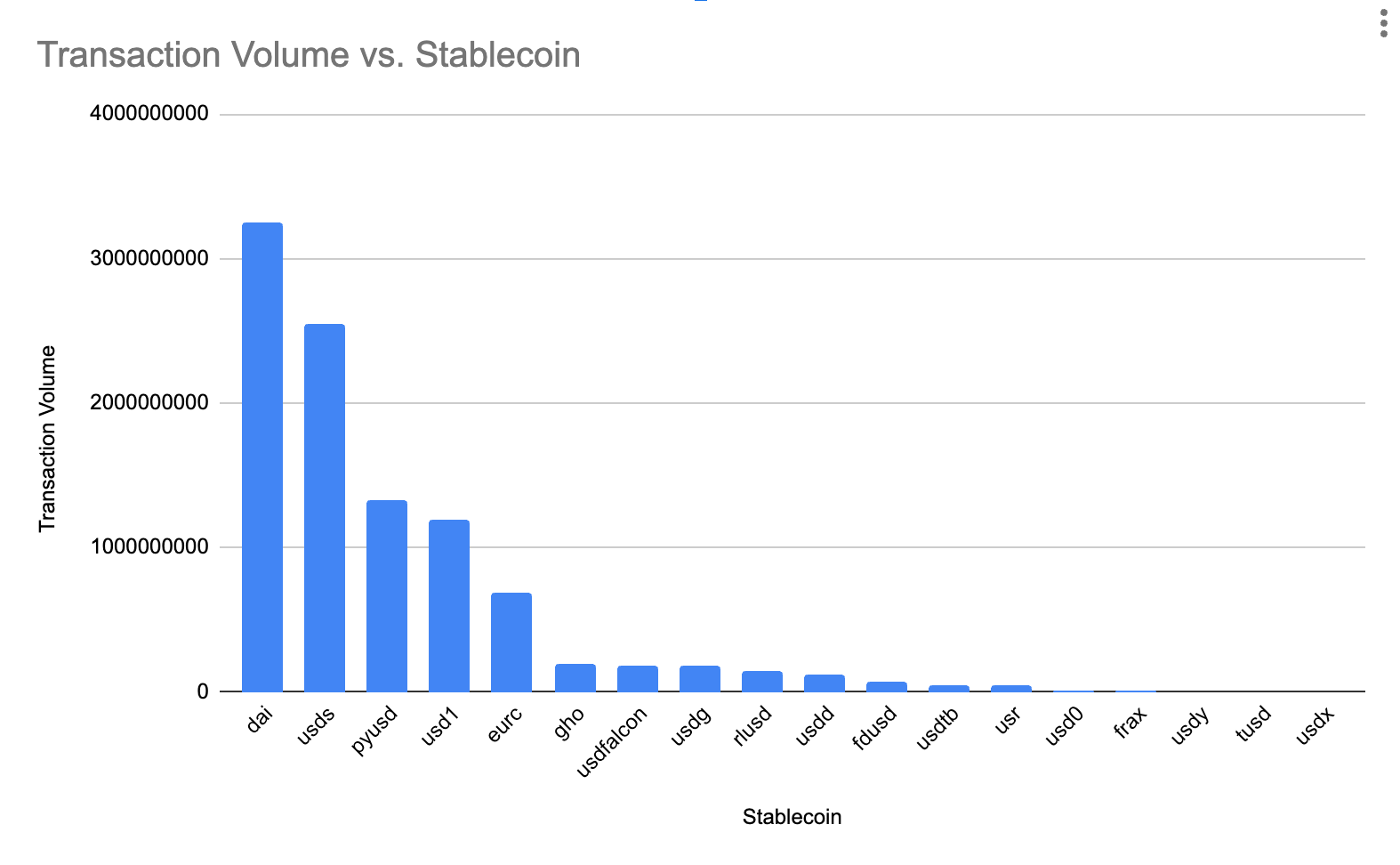

What happens if we use transaction volume?

Once again feels a bit apples to oranges in terms of underlying use cases. Viewing the data this way also makes me worry that you catch big movements related to mint/burn rather than approximate usage. A new partner coming in, minting $100M and then moving it 3-4 times on-chain can make that stablecoin suddenly number one in this category.

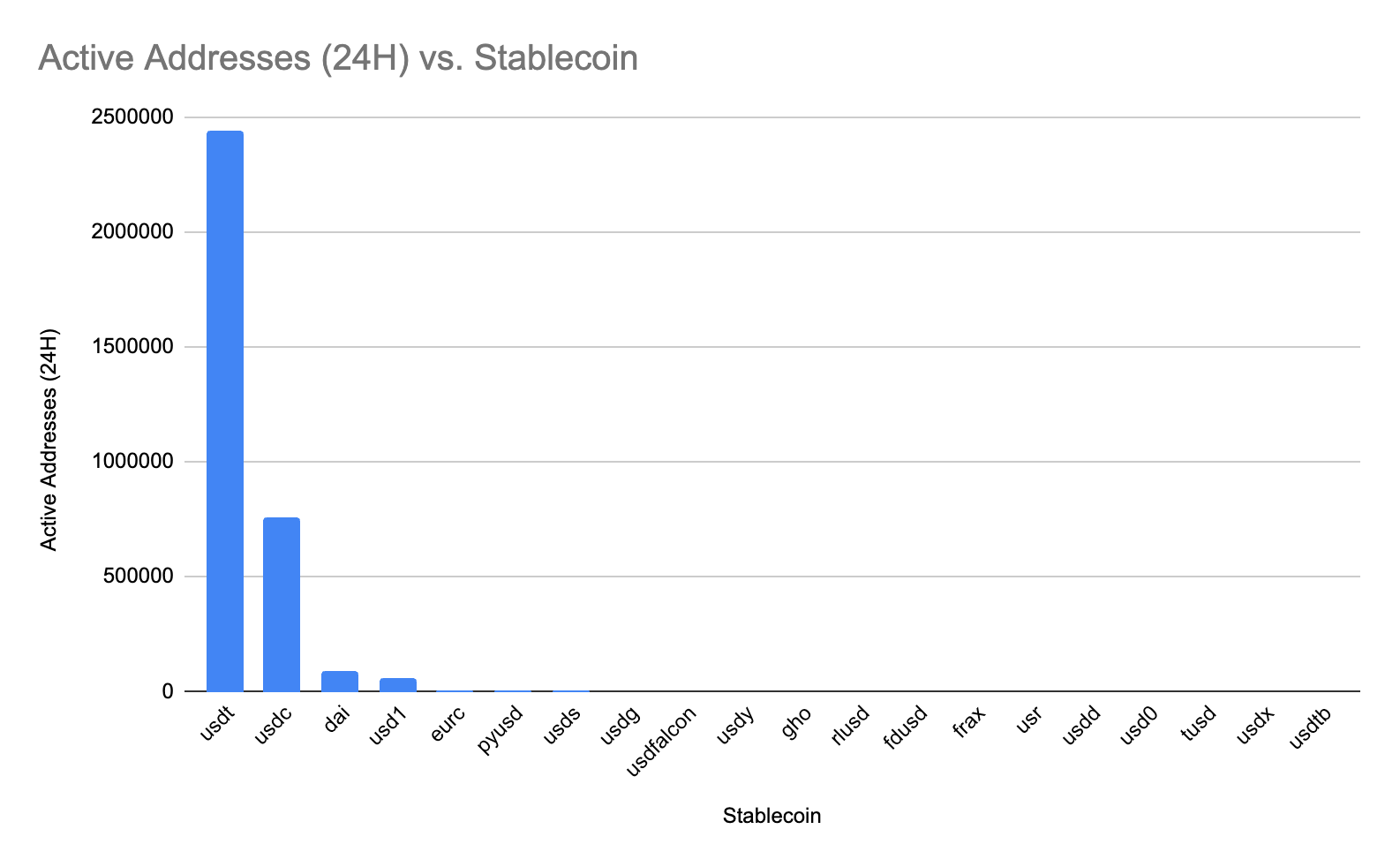

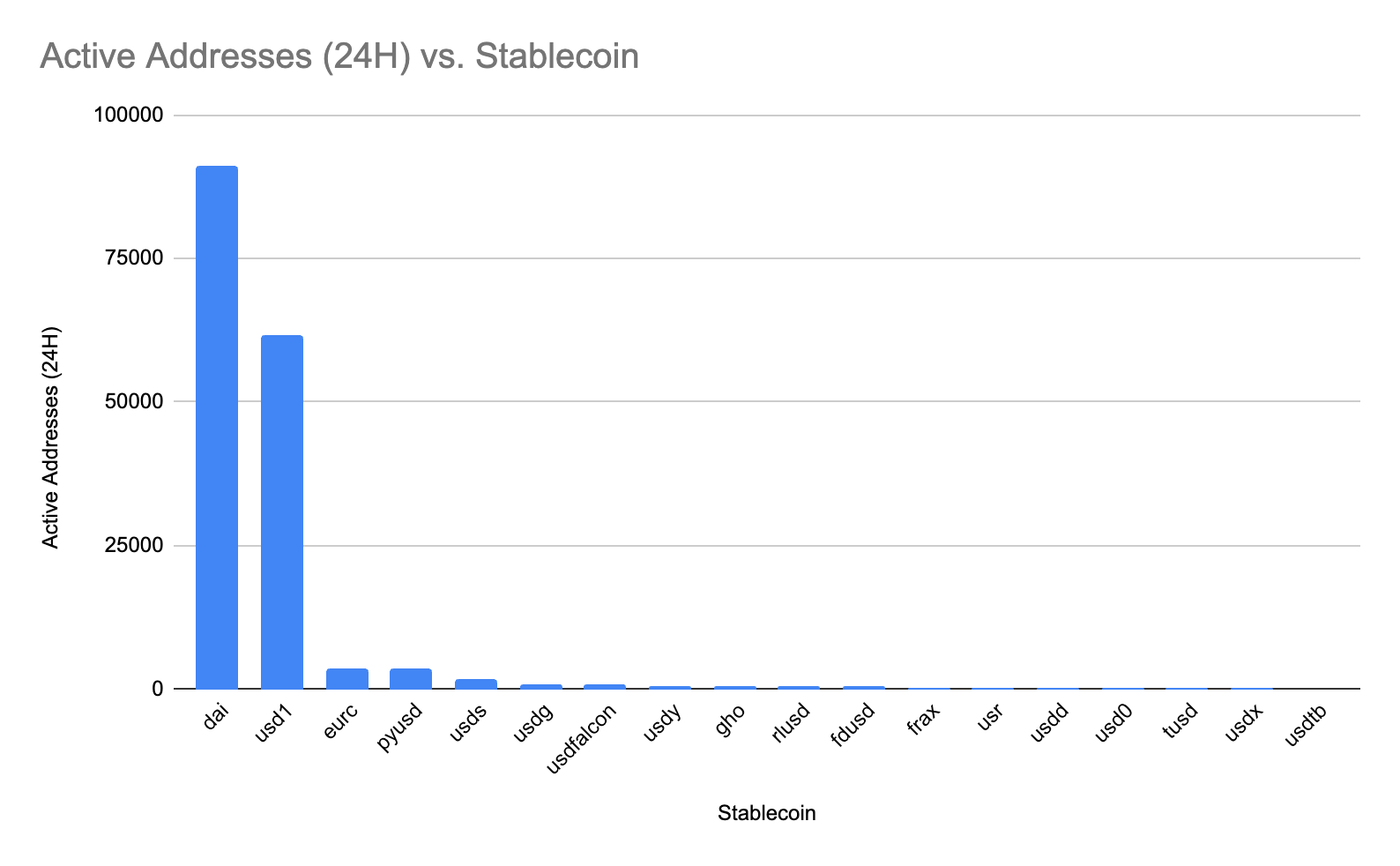

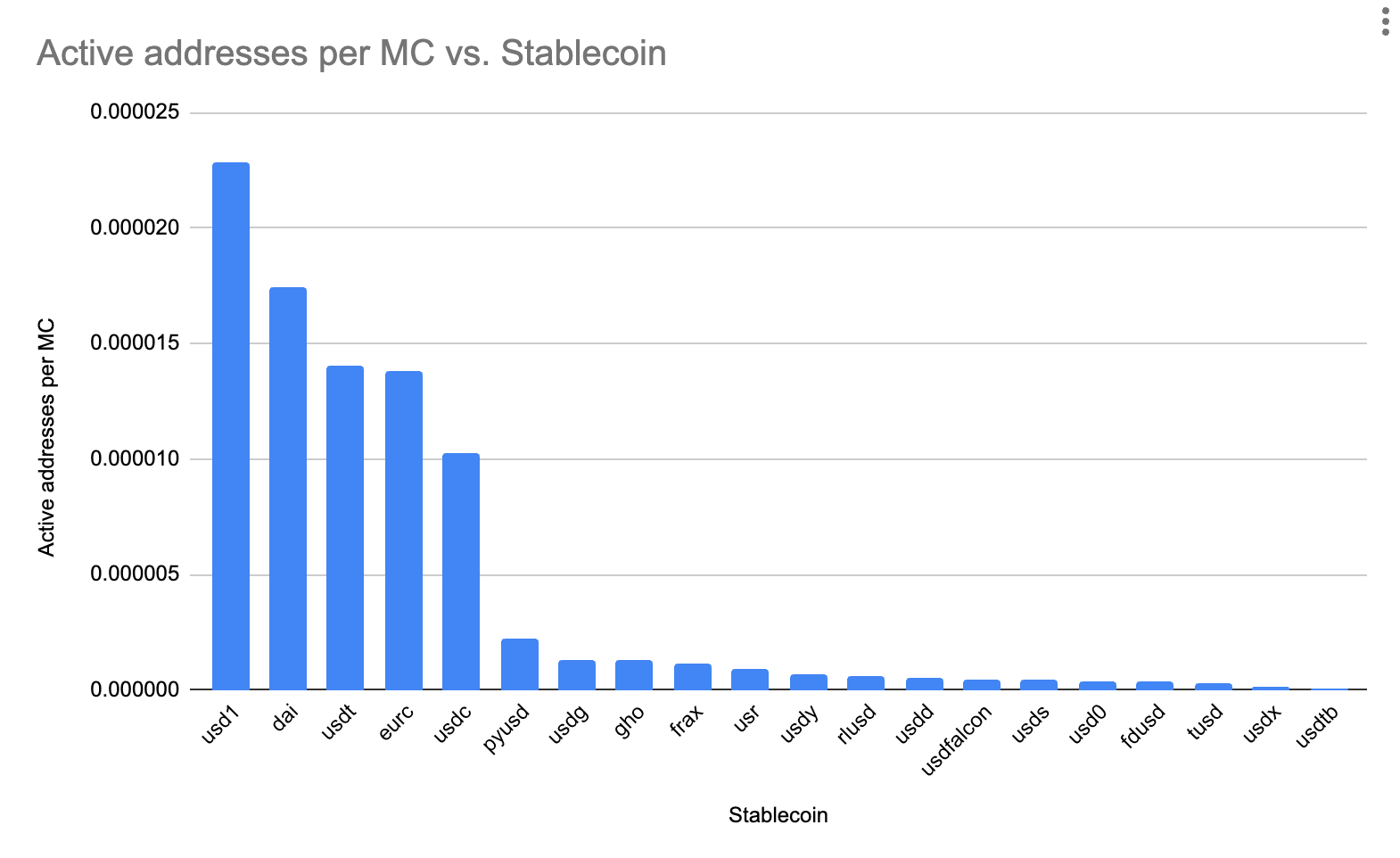

What happens if we use active addresses?

Apples to oranges thing again of course but here I also wonder if the way some big on-chain destinations structure their wallets is more of a factor. For instance if one CEX holds the funds of 1M users omnibus, they might only count as a single active address. The opposite is true in other places.

What about different ratios relative to market cap?

This is a slightly better way to think about the problem but a lot of the problems mentioned above persist.

Conclusion

Overall this exploration was not particularly satisfying. I’m posting this because I said I would, not because I think it is good or insightful. I’m also posting in hopes someone builds (or points me towards) better dashboards that track these things over time.

There are just too many factors at play here to find a single metric to determine “best” in terms of stablecoins.

The next iteration on this would be to evaluate on a per use case basis which metrics matter and then look at those metrics relative to which stablecoin might win that use case long term.

AUM = Assets Under Management which in itself probably isn’t a perfect definition. Market cap is a better term but I’m going to use it interchangeably with AUM because acronyms are easy to write. AUM is technically the backing assets of the stablecoin itself. In most case cash and cash equivalents (US Treasuries).

This is insane and not insane at the same time. $500B valuation would make Tether the 20th largest company compared to publicly traded ones. But based on revenue this is fairly middle of the road reasonable. But is the revenue sustainable? Will something else come along and become number one? Time will tell.

Or least bad

At a simple level, revenue for an issuer is [market cap] x [yield generated by backing assets] x [% of yield not distributed to partners]. The not simple part is the amount of yield generated back to partners is very opaque and ranges from 0 to 100% depending on the issuer.

It seems unlikely we will see extrajudicial action on the part of a regulator again in the US, but you never know.

I’m generally of the school of thought that despite owning 90%+ of the market, Tether and Circle have definitely not won. It is still too early.

At least not easy for me to figure out for a post. If someone wants to go figure these out it is definitely possible and I’ll retroactively link to it.

You could figure revenue out pretty closely through marketing materials but costs (an in particular marketing costs) are nearly impossible to figure out consistently.

Largely publicly available but impossible to quantify.

This matters so much for going mainstream. Having worked in an environment where this was our priority it is frustrating that Circle CEO Jeremy Allaire totally got away with saying “Circle is regulated” for years when in reality they only had money transmitter licenses (MTLs) which no reasonable person would ever say is regulation.

I’m sure some good studies for brand awareness and reputation exists but I couldn’t come across any that covered what I was looking for.

Sort of self-fulfilling because if a stablecoin gets big enough this largely gets solved and if a stablecoin can’t solve for this it isn’t going to get very big.

If you assume the regulated stablecoins are adhering to regulations (and if they aren’t why did they bother going through all that effort) then you can figure this out. For the others you just have to sort of trust them. The “just trust us” argument is tough when a few years ago Tether was making headlines for the extent of their backing assets that were possibly tied up in Chinese based commercial paper.

Again “just trust us”

This would be interesting to dive into. If DeFi is the future, smart contract usage could be a really good way to get a sense of which stablecoin wins in DeFi.

On one hand everyone is the same if they are backed by cash and cash equivalents. It is whatever the effective Fed funding rate (EFFR) is at a given moment. On the other hand basically everyone is adding marketing incentives on top of this yield which have a million caveats so it becomes impossible to compare.

Everyone is spending to grow but no one will ever admit to how much.

So much of the activity in crypto is trading, this is possible to quantify but the way the data and exports from sites like CoinGecko and CoinMarketCap work, it takes too long to filter out bad data and be confident in the results.

Chain or network or protocol. It always strikes me as surprising about how these terms are all more or less used interchangeably but also mean different things.

This specific view for simplicity. The way it counts last 24 hours has me scratching my head a bit but I need to strike a balance between how quickly I could compile data vs having the perfect data.

If you are reading this and want to do this, I’ll link to it retroactively.

Assuming USDC doesn’t grow further and these rates of growth are sustained. Both assumptions seem unreasonable.